The Purchase Cost, Insurances, Maintenance Expenses and Property Taxes for your Florida Property

The purchase price of a property plays a big role when you think about buying real estate.

Equally important, however, is to know what the associated costs will be, so your final number will take everything into consideration.

The fees can vary, especially when it comes to financing a single family home. Exact amounts can only be determined if the individual situation is assessed. The numbers stated below are based on a home purchase price of $400,000 an state the typical purchase and financing expenses.

Purchase Cost and Expenses (Cash)

- Title Insurance: paid by seller if not negotiated otherwise

- Settlement Fee of Title Company: usually less than $200

- Attorney's Fees: in case you want your attorney to review the offer and/or contract

- Recording Fees: approx. $20

- Home Inspection: approx. $350 to $900 depending on the size of the home and the inspections (Termites, Chinese Drywall, Mold, 4-point, Wind Mitigation etc.)

- Lot Survey: approx. $450 to $650 (depending on the type of survey, i.e. boundary or building survey)

- Proration of property taxes: will be prorated accurately down to the day

- Assessments: This only results in a cost if these are being assumed and possibly paid off at the closing

The total cost of purchasing a property therefore should be approx. $1,000 in most of the cases.

Financing Purchase Expenses

- Origination fee: approx. $775

- Appraisal, Elevation Certificate, Credit Report, Recording fees: approx. $500

- Lender's Title Insurance, Home Inspection, Survey, Attorney fees: approx. $1,100

- Buyer's Title Insurance: approx. $2,100

- Translation fees (if needed for a foreign national): approx. $600

- Homeowner and Flood Insurance: approx. $2,500

- Fees of Title Company: usually less than $500

- Doc stamps on mortgage and recording fees: approx. $1,700

- Proration of property taxes: will be calculated down to the day

- Assessments: This only results in expenses if they are assumed and paid off at the time of closing

In this example the closing cost are approx. $11,000 for the buyer.

All numbers are estimated and can vary from bank to bank

Proration of the property taxes

|

Property tax of the lot or home for the year: |

$2,760.00 |

|

Closing date: |

April 30th |

|

Number of days seller owned property (Jan1-April 30) |

120 days |

|

Calculation based on 360 days per year: 2760:360x120 Seller's prorated amount of the property tax: |

$ 920.00 |

The Seller is debited with the amount while the Buyer receives a tax proration credit on the Settlement Statement at closing in the amount of $920.00. At the end of the year the buyer has to pay the full year tax. This way he effectively only paid the difference of $1,840.00 for the 8 months he owned it starting May 1st.

Insurances for your home in Florida

The Homeowner Insurance

1. Dwelling Insurance

This insures the actual building and everything that is affixed to it, like the swimming pool, the built-in kitchen or the outside compressor of the air-conditioning system. This is the so called dwelling coverage. However you have to make sure that other than the pool you also have coverage for the pool screen, as some insurance carriers do not automatically include it. In a claim situation this would not be covered then.

2. Personal Property Insurance

This personal property insurance protects you with regards to all mobile property, that is not attached to the home, e.g. the furnishings, electrical and electronic devices, clothing etc. Precious items like jewels or any type of art usually have to be insured by a separate policy as it is never included in the regular personal property insurance.

Most of the insurance companies also offer an optional liability insurance which covers any damage or injury that people suffer that do not belong to your household. Even legal cost associated with that will be taken care of.

It is important to know that all policies with have a deductible included. This serves to make sure that for smaller claims the homeowner himself steps in and pays for it. Any amount beyond the deductible is then covered through the insurance policy. These deductibles are structured differently, e.g. in a claim resulting from a storm the deductible is 2% of the building value (hurricane deductible) whereas damages coming from other sources (“all other perils”) mostly have a deductible of $1,000.

Insurance companies mostly offer lower premiums if the homeowner is willing to increase the deductible to 5% or even 10%. On the other hand you can also choose to have no deductible at all which of course will increase the insurance premium.

Flood Insurance

Flood Insurance

Any damages pertaining to a flood are not covered by the dwelling insurance. In case you are financing your purchase and your property is located within a flood zone, the bank will require flood insurance as it is mandatory.

The Federal Emergency Management Agency (FEMA) determines the areas in which flooding is likely and the probability of the flooding risk, therefore properties located in different flood zones will be less or more expensive to insure. It is always recommendable to get flood insurance.

As of October 1, 2021 FEMA updated the National Flood Insurance Program's (NFIP) risk rating methodology through the implementation of a new pricing methodology call Risk Rating 2.0. It levers industry best practices and cutting-edge technology to enable FEMA to deliver rates that are actuarily sound, equitable, easier to understand and better reflect a property's flood risk.

In the past lower-valued homes paid more than their share of the risk and higher-valued homes paid less than their share. With the new NFIP 2.0 this is adjusted for everyone to pay their fair share according to the property they own.

Are condos treated the same way?

Condos in most of the cases are partly insured by the Homeowner Association (HOA) or Condo Association.

However if the tenant or owner wants to protect personal property it has to be done through a separate policy. Moreover you should know that the master policy of the Condo or Homeowner Association only covers the outside portion of the building, meaning outside walls, roof etc. Everything on the inside of the building, for example the inside walls, ceilings and floors have to be part of the tenant's/owner's insurance policy.

Does it matter how I use my home or condo?

All insurance carriers want to know exactly how you will use your home or apartment, meaning will it be your primary residence, second home or a seasonal residence. As an example: A seasonal residence can be vacant for up to 9 months. If a homeowner wants to have coverage for short term rentals then this will have to be incuded in the policy as well.

Can I insure my seawall or boat dock as well within my homeowner insurance?

Seawalls in general cannot be insured, however boat docks can be part of the homeowner insurance if they are made part of “other structures” within the policy.

What about lots?

Unimproved land can be insured as well. If an owner holds multiple parcels in his own name he could also use an umbrella policy to cover them all.

This information only serves to give a general idea about insurances. It is in no way to be considered insurance advice. Please contact a licensed insurance agent in order to get all details for your individual situation.

Maintenance Expenses for your home in Florida

Maintenance related expenses are a major factor in the decision making process of a buyer no matter if it is used as the primary residence or a vaction home.

In case of a vacation home most buyers want to have it looked after by a professional property management company. Here you can find a list of typical costs for a home / vacation rental (example of a home valued at $650,000):

- Property Management: approx. $150 (this includes payment of invoices, weekly check of the property)*

- Rentals: No direct cost as everything comes out of the rental income

- Pool Service: approx. $90*

- Lawn Service: approx. $95 (includes trimming of bushes)

- Lawn fertilization: approx. $40*

- Pest Control: approx. $40

- Electricity: approx. $150 - $250 (this depends on the installed appliances and devices as well as vacany of the home)

- Water: approx. $95 (2 person usage)

- Phone, Internet, TV: approx. $180*

- Flood Insurance: starting at $750 (depending on the flood zone where the home is located in)

- Homeowner Insurance: approx. $1,700 - $4,000 (depending on the age of the home and the code it was built to)

- Property tax: approx. $9,500 (depending on the assessed value of the property)

For the property tax you can use these approximate percentages of the assessed value (Important: The assessed value most of the time is a lot lower than the market value / purchase price:

- Home with riverfront, assessed value $1,000,000 = approx. 2.25%

- Home on gulf access canal, assessed value $600,000 = approx. 2%

- Home on freshwater canal, assessed value $350,000 = approx. 1.5%

- Home on dry lot, assessed value $200,000 = approx. 1% - 1.25%

Should you purchase a home or condo within a gated community some of the expenses may be part of the HOA fees like water, TV, lawn and pool service etc.

In general most of the homes in this price segment of $600,000 to $700,000 will have expenses in the amount of $20,000 or more. Smaller homes will have less property taxes and therefore reduced expenses. How a vacation home, even with these high expenses, can still be a good investment is shown in these rental scenarios.

*These positions do not necessarily have to be considered in some cases

All listed costs are estimated and can vary due to location, age, size and features of the property

The Property Taxes

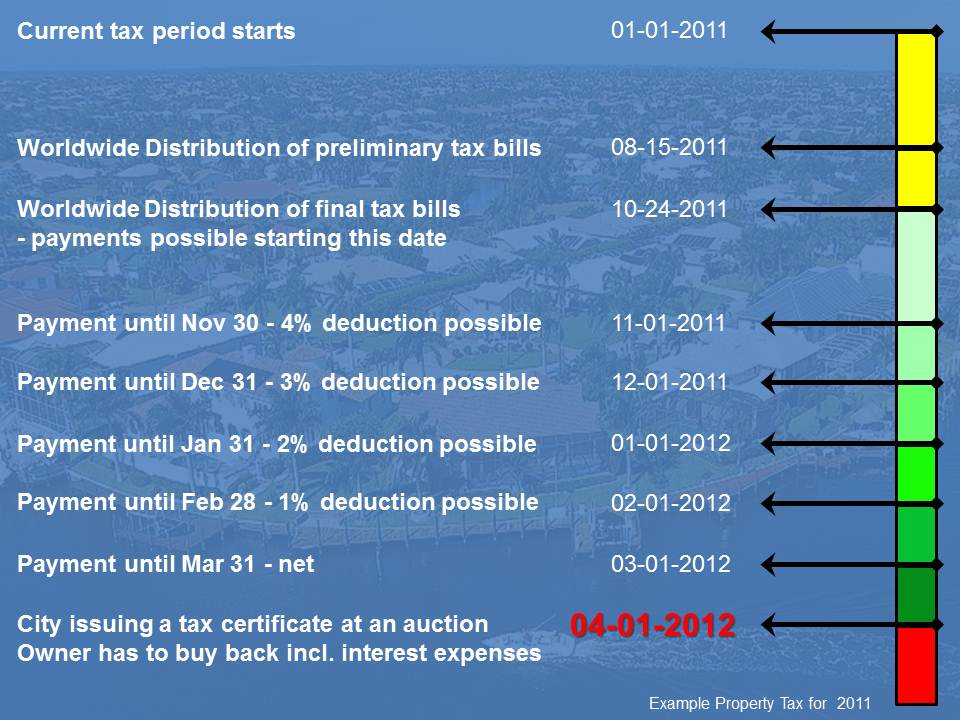

The annual property tax bills will be sent out by the city for the current year. A tax assessment notice is usually distributed in August already whereas the final tax bill will be delivered to property owners in the last week of October of every year. Often there are questions about how they are being calculated and what the single items mean. This page should allow for a better understanding.

The annual property tax bills will be sent out by the city for the current year. A tax assessment notice is usually distributed in August already whereas the final tax bill will be delivered to property owners in the last week of October of every year. Often there are questions about how they are being calculated and what the single items mean. This page should allow for a better understanding.

First of all the city will determine the total tax budget needed. After that the values of all properties will be assessed. The city administration consists of different authorities, e.g. the authority responsible for police and fire departments, schools, libraries, waste removal, mosquito control, water management, waterways etc. that all show their own portion of the taxes in the bill.

Let's assume that the total planned city budget is $280 million for the next year and that the assessed value of all properties within the city boundaries is $20 billion. The budget is being divided by the total value which results in a so called millage rate of 0.014. We further assume that your property is being assessed at $250,000 by the General Appraiser. This amount is being multiplied with the millage rate: $250,000 x 0.014 = $3,500. Your property tax will then be $3,500 per year. The General Appraiser only assesses the value of the properties, but not the millage rate. In the tax bill you will see all the single line item positions.

Payment

All final tax bills will be sent to the owners recorded address during the last week of October. They are due on March 31st of the following year. You can save money by paying early. The city offers you a discount of 4% just by settling the account in November. Each month you will be able to deduct 1% less until you have to pay the net amount in March. If you have not paid by the end of March you risk that the city will issue a tax certificate to get the money from somebody else. To not lose any interest in your property you have to buy back this certificate from that person including fees and the additional interest accumulated.

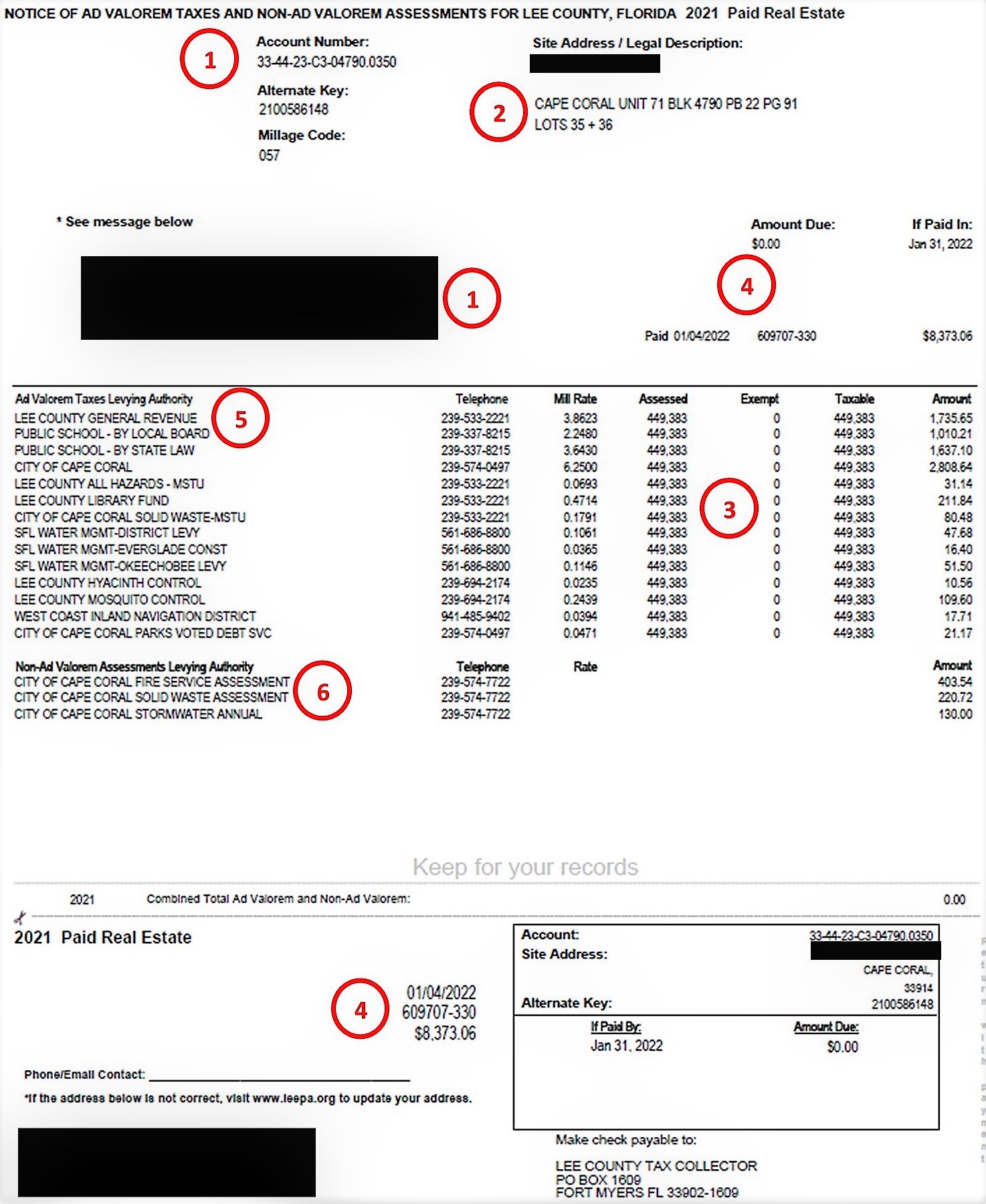

Line items of the Property Tax Bill

Line items of the Property Tax Bill

1. Account number, name, site address and recorded address of the owner

2. Legal description of the property

3. Market assessed and cap assessed value and deductions for homestead, blind people, widows etc. and the final taxable value

4. Amounts due depending on date of payment

5. (Ad valorem=value is the base) Taxes of levying authorities and millage rates as well as exemptions and final amount

6. (Non-Ad valorem=size is the base) Assessments for fire service, solidwaste and financed city utilities but also stormwater fees and mowing fees for unimproved lots

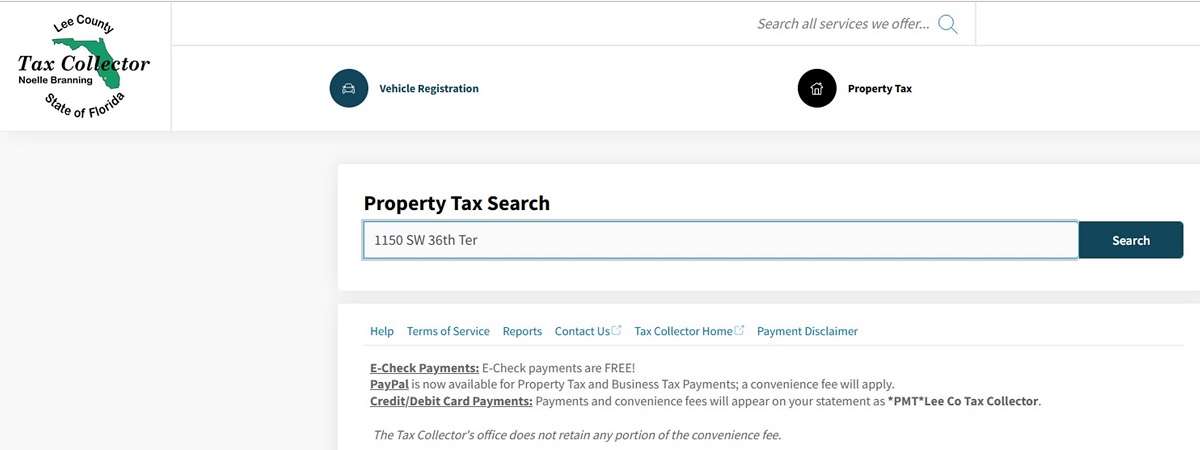

You can pay property taxes by credit card at any time on the Lee County Tax Collector's website. All you have to do is go to https://lee.county-taxes.com/public/search/property_tax. Then enter the address in the PROPERTY TAX SEARCH field, e.g. 1150 SW 36th Ter and click on Search.